Kontakt

Kontakt Kako nakupovati

Kako nakupovatiDostava

Svetovalec pri nakupu

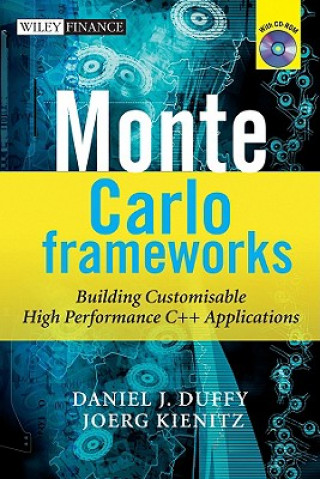

Monte Carlo Frameworks - Building Customisable High-Performance C++ Applications

Angleščina

Angleščina

225 b

225 b

30 dni za vračilo blaga

Drugi so kupili tudi

/

/

Mehka

Mehka

17.51

€

17.51

€

/

Mehka

8.90

€

/

Mehka

8.90

€

"With many books on C++ and Monte Carlo methods at hand, Daniel and Jörg have taken a serious approach to combine these topics in one volume. It is this combination that makes the book worth reading for a junior quant as an introduction and for a senior quant as a reference guide of some of the recent developments in financial engineering. The authors cover the basic models used mainly in equity derivatives up to stochastic volatility, jump diffusions and Lévy processes. The Monte Carlo method contains computation of Greeks, many variance reduction methods and handling early exercise features. This way the reader can learn the theory and the implementation in C++ (the industry standard in financial engineering) including using the boost library, standard template library (STL) up to building own libraries (DLLs and XLLs). Many case studies with lists of results and numerous exercises make it easy to learn and verify the valuation of financial instruments. You can start your career to become a good quant by reading this book."§Uwe Wystup, Managing Director of MathFinance AG.§"The reader is presented with a clear and readable self-contained guide for the Monte Carlo framework in C++. It discusses the complete software lifecycle of the Monte Carlo simulation process for computational finance and will therefore be directly useful for the quant and academic community. For sure a hands-on standard reference."§Wim Schoutens, Research Professor Financial Engineering, Catholic University of Leuven.This is one of the first books that describe all the steps that are needed in order to analyze, design and implement Monte Carlo applications. It discusses the financial theory as well as the mathematical and numerical background that is needed to write flexible and efficient C++ code using state-of-the art design and system patterns, object-oriented and generic programming models in combination with standard libraries and tools.§Includes a CD containing the source code for all examples. It is strongly advised that you experiment with the code by compiling it and extending it to suit your needs. Support is offered via a user forum on www.datasimfinancial.com where you can post queries and communicate with other purchasers of the book.§This book is for those professionals who design and develop models in computational finance. This book assumes that you have a working knowledge of C ++.The Monte Carlo method is now acknowledged as being one of the most robust tools for a range of applications in finance, from option pricing to risk management and optimization. One of the best languages for the development of Monte Carlo applications and frameworks is C++, an object-oriented and generic programming language which is also an industry standard.§This is one of the first books that describe all the steps that are needed in order to analyze, design and implement Monte Carlo applications. It discusses the financial theory as well as the mathematical and numerical background that is needed to write flexible and efficient C++ code using state-of-the-art design and system patterns, object-oriented and generic programming models in combination with standard libraries and tools.§The book is divided into four parts, each one dealing with one major aspect of the current problem domain. The features and topics are:§Option pricing for a range of one-factor and n-factor models;§European, Asian, baskets, Heston, jump models;§Early exercises, calculating option sensitivities;§The mathematical theory of n-factor Stochastic Differential Equations (SDE);§An introduction to the numerical analysis of SDE;§Modelling SDE and the Finite Difference Method (FDM) in C++;§Applying design and system patterns (GOF, POSA) for improved design;§Extensive use of the STL and boost libraries;§Multi-threading and parallel programming (OpenMP) techniques for Monte Carlo;§Creating Excel-based applications using xlw, Automation and COM;§Extra discussion of mathematical foundations for Monte Carlo;§Working source code is provided along with numerous examples, exercises and projects related to the extension of the C++ framework.§The book is accompanied by a CD which contains the source code for all the examples. It is strongly advised that you experiment with the code by compiling it and extending it to suit your needs. Support is offered via a user forum on www.datasimfinancial.com where you can post queries and communicate with other purchasers of the book.

O knjigi

Angleščina

Podarite to knjigo še danes

To je povsem preprosto

1 Dodajte knjigo v košarico in izberite dostavo kot darilo 2 V zameno vam bomo poslali kupon 3 Knjiga bo dostavljena na naslov obdarovancaMorda bi vas zanimalo tudi

/

Mehka

19.23

€

/

Mehka

19.23

€

Pozdravljeni! Sem Libroamiko, vaš knjižni svetovalec.

Kako vam lahko pomagam?