Brezplačna dostava za naročila nad 69,99 € na prevzemna mesta DPD in Express One.

Postanite del skupnosti ljubiteljev knjig z vsega sveta in uživajte v številnih ugodnostih.

Ustvarite brezplačen račun

Brezplačna dostava Zásilkovna nad 69.99 €

Zbirna točka GLS 4.49 €

Zbirna točka DPD 2.99 €

Kurirska služba GLS 5.49 €

Kurir DPD 3.49 €

Kurirska služba Express One 3.49 €

Zbirno mesto Express One 3.49 €

Zbirno mesto Pošte Slovenije 3.49 €

Dostava preko Pošte Slovenije 3.49 €

Kontakt

Kontakt Kako nakupovati

Kako nakupovati

Pomoč

Dostava

Zbirna točka GLS 4.49 €

Zbirna točka DPD 2.99 €

Kurirska služba GLS 5.49 €

Kurir DPD 3.49 €

Kurirska služba Express One 3.49 €

Zbirno mesto Express One 3.49 €

Zbirno mesto Pošte Slovenije 3.49 €

Dostava preko Pošte Slovenije 3.49 €

Brezplačna dostava Zásilkovna nad 69.99 €

Svetovalec pri nakupu

Moj račun

▸

Prazna :-(

0

Brezplačna dostava za naročila nad 69,99 € na prevzemna mesta DPD in Express One.

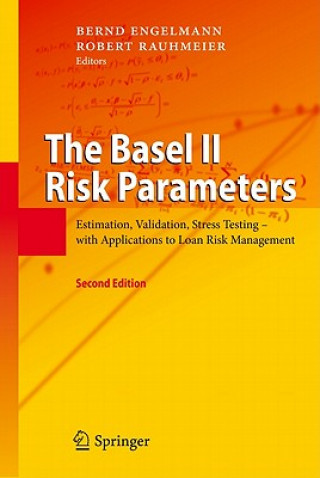

Basel II Risk Parameters

Estimation, Validation, Stress Testing - with Applications to Loan Risk Management

Jezik

Angleščina

Angleščina

Angleščina

Knjiga

Trda

The estimation and validation of the Basel II risk parameters PD (default probability), LGD (loss gi...

Celoten opis

Koda Libristo: 01656741

?

253 b

253 b

253 b

104.69

€

Na zalogi pri dobavitelju

Odposlali bomo v 10-13 dneh

Do 30 dni za vračilo

Drugi so kupili tudi

/

/

binding.

binding.

60.38

€

60.38

€

The estimation and validation of the Basel II risk parameters PD (default probability), LGD (loss given default), and EAD (exposure at default) is an important problem in banking practice. These parameters are used on the one hand as inputs to credit portfolio models, on the other to compute regulatory capital according to the new Basel rules. The book covers the state-of-the-art in designing and validating rating systems and default probability estimations. Furthermore, it presents techniques to estimate LGD and EAD. A chapter on stress testing of the Basel II risk parameters concludes the monograph.

Igralka

&

Poliglotka

EWA KASP

za

Predvajaj video

Libristo ima največjo izbiro tujejezične literature. Zato svoje knjige kupujem tukaj.

O knjigi

Polni naslov

Basel II Risk Parameters

Avtor

Bernd Engelmann, Robert Rauhmeier

Jezik

Angleščina

Angleščina

Vezava

Knjiga - Trda

Datum izida

2011

Število strani

426

EAN

9783642161131

ISBN

3642161138

Koda Libristo

01656741

Teža

750

Mere

158 x 241 x 29

Podarite to knjigo še danes

To je povsem preprosto

1 Dodajte knjigo v košarico in izberite dostavo kot darilo 2 V zameno vam bomo poslali kupon 3 Knjiga bo dostavljena na naslov obdarovancaMorda bi vas zanimalo tudi

/

Mehka

14.05

€

/

Mehka

14.05

€

Knjižni svetovalec Libroamiko

Z uporabo tega klepeta komunicirate z generativno umetno inteligenco. Z njegovo uporabo se strinjate tudi z obdelavo osebnih podatkov.

Pozdravljeni! Sem Libroamiko, vaš knjižni svetovalec.

Kako vam lahko pomagam?

Pozdravljeni, sem Libroamiko, vam lahko pomagam?